The smart Trick of Chapter 7 Vs Chapter 13 Bankruptcy That Nobody is Talking About

The smart Trick of Chapter 7 Vs Chapter 13 Bankruptcy That Nobody is Talking About

Blog Article

The Greatest Guide To Chapter 7 - Bankruptcy Basics

Table of ContentsThe Of Experienced Bankruptcy Lawyer TulsaBankruptcy Law Firm Tulsa Ok Things To Know Before You Get ThisSome Ideas on Chapter 7 - Bankruptcy Basics You Should KnowThe smart Trick of Tulsa Debt Relief Attorney That Nobody is DiscussingWhat Does Tulsa Ok Bankruptcy Attorney Mean?

The stats for the other main kind, Phase 13, are even worse for pro se filers. Suffice it to claim, speak with a lawyer or two near you that's experienced with bankruptcy law.Several attorneys likewise offer cost-free examinations or email Q&A s. Take advantage of that. Ask them if personal bankruptcy is undoubtedly the right choice for your circumstance and whether they believe you'll qualify.

Advertisement Now that you've made a decision insolvency is certainly the best course of activity and you with any luck cleared it with an attorney you'll need to obtain begun on the paperwork. Before you dive right into all the official insolvency kinds, you must get your very own papers in order.

The Ultimate Guide To Tulsa Bankruptcy Attorney

Later down the line, you'll in fact need to show that by divulging all kinds of information about your financial events. Below's a fundamental list of what you'll require on the roadway in advance: Identifying documents like your motorist's permit and Social Security card Income tax return (as much as the past 4 years) Evidence of income (pay stubs, W-2s, self-employed earnings, revenue from properties in addition to any kind of income from government advantages) Bank statements and/or retired life account statements Proof of value of your properties, such as automobile and realty assessment.

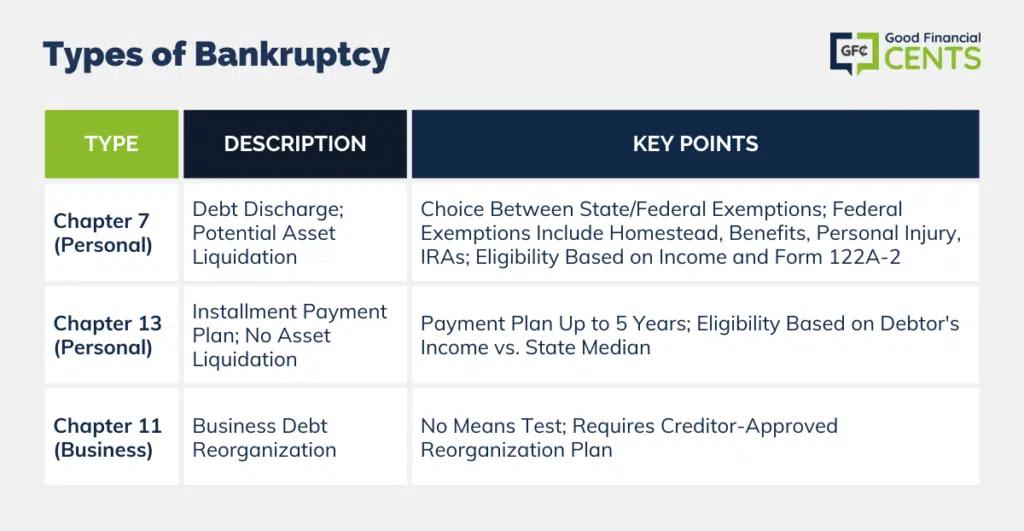

You'll want to comprehend what kind of financial debt you're trying to deal with.

You'll want to comprehend what kind of financial debt you're trying to deal with.If your revenue is expensive, you have one more option: Chapter 13. This alternative takes longer to resolve your debts since it needs a lasting repayment strategy usually three to five years before a few of your remaining debts are cleaned away. The filing procedure is also a great deal a lot more complicated than Phase 7.

The Ultimate Guide To Chapter 7 Bankruptcy Attorney Tulsa

A Phase 7 insolvency remains on your credit scores report for 10 years, whereas a Phase 13 personal bankruptcy drops off after 7. Before you submit your insolvency forms, you have to first complete an obligatory training course from a debt therapy firm that has actually been authorized by the Division of Justice (with the noteworthy exemption of filers in Alabama or North Carolina).

The training course can be finished online, face to face or over the phone. Training courses typically set you back in between $15 and $50. You need to complete the program within 180 days of filing for personal bankruptcy (Tulsa bankruptcy attorney). Make use of the Division of Justice's website to discover a program. If you live in Alabama or North Carolina, you have to select and finish a training course from a listing of individually accepted suppliers in your state.

Top Tulsa Bankruptcy Lawyers Things To Know Before You Buy

Inspect that you're submitting with the appropriate one based on where you live. If your long-term official statement house has actually relocated within 180 days of filling up, you should file in the area where you lived the better portion of that 180-day period.

Generally, your personal bankruptcy attorney will collaborate with the trustee, however you may require to send out the individual files such as pay stubs, tax obligation returns, and financial institution account and credit history card declarations straight. The trustee who was just selected to your case will certainly quickly establish a required conference with you, referred to as the "341 meeting" since it's a requirement of Area 341 of the U.S

You will require to offer a timely listing of what qualifies as an exemption. Exemptions might put on non-luxury, main vehicles; required home items; and home equity (though these exemptions guidelines can differ widely by state). Any type of building outside the list of exceptions is taken into consideration nonexempt, and if you do not provide any type of checklist, after that all your building is taken into consideration nonexempt, i.e.

You will require to offer a timely listing of what qualifies as an exemption. Exemptions might put on non-luxury, main vehicles; required home items; and home equity (though these exemptions guidelines can differ widely by state). Any type of building outside the list of exceptions is taken into consideration nonexempt, and if you do not provide any type of checklist, after that all your building is taken into consideration nonexempt, i.e.The trustee would not market your cars to quickly pay off the financial institution. Rather, you would pay your lenders that amount throughout your repayment strategy. An usual misconception with bankruptcy is that once you submit, you can quit paying your financial debts. While personal bankruptcy can aid you erase much of your unsecured financial debts, such as past due medical bills or personal fundings, you'll want to maintain paying your regular monthly payments for guaranteed debts if you desire to keep the visit the website residential or commercial property.

Tulsa Bankruptcy Legal Services for Dummies

If you're at risk of foreclosure and have actually worn down all various other financial-relief options, after that applying for Chapter 13 may postpone the repossession and conserve your home. Ultimately, you will still require the income to continue making future home mortgage repayments, along with repaying any type of late repayments throughout your payment strategy.

The audit could delay any type of financial debt relief by a number of weeks. That you made it this much in the process is a good indicator at the very least some of your debts are qualified for discharge.

Report this page